Free Car and Motor Insurance quotation on line. You can now purchase Car and Motor Insurance online also. Find out more.

What you need to know all about Personal Financial Planning, Risk Management , Wealth Accumulation, Wealth Creation, Wealth Preservation and Wealth Distribution. How and what to do for children education funding, retirement funding and etc ? Where to find help and advice and who to approach ? You can send in your enquiry to email: ttong3@gmail.com or call +603-20817435 or chat without any obligation.

Showing posts with label Promotions. Show all posts

Showing posts with label Promotions. Show all posts

Thursday, October 7, 2021

Monday, December 31, 2018

Wednesday, April 4, 2018

Zurich SureCover

Zurich Life Insurance Malaysia Berhad just launched a new product call Zurich SureCover.

This is the enhance of our current existing product call Senior Gold. Senior Gold policy is for those age 50 to age 80 whereas this Zurich SureCover is from age 35 to age 80. This is good news for those who can't get insurance due to their medical conditions, which means we will never turn down your application regardless of your health condition.. This is a whole life insurance policy and is guaranteed acceptance and coverage until age 100. Each unit cost Rm75 per month with a insurance coverage of Rm33,085 for age 35 and if accidental death occurs it pay up to 5 times of the Basic Sum Insured.

This is the enhance of our current existing product call Senior Gold. Senior Gold policy is for those age 50 to age 80 whereas this Zurich SureCover is from age 35 to age 80. This is good news for those who can't get insurance due to their medical conditions, which means we will never turn down your application regardless of your health condition.. This is a whole life insurance policy and is guaranteed acceptance and coverage until age 100. Each unit cost Rm75 per month with a insurance coverage of Rm33,085 for age 35 and if accidental death occurs it pay up to 5 times of the Basic Sum Insured.

Tuesday, October 10, 2017

3H

Today this insurer promote their 3 Highs. Those with High Blood Pressure, High Cholesterol and High Body Mass Index that cannot get insurance from others insurer , can apply to this company . Need advise on how to go about , pm me.

Monday, October 9, 2017

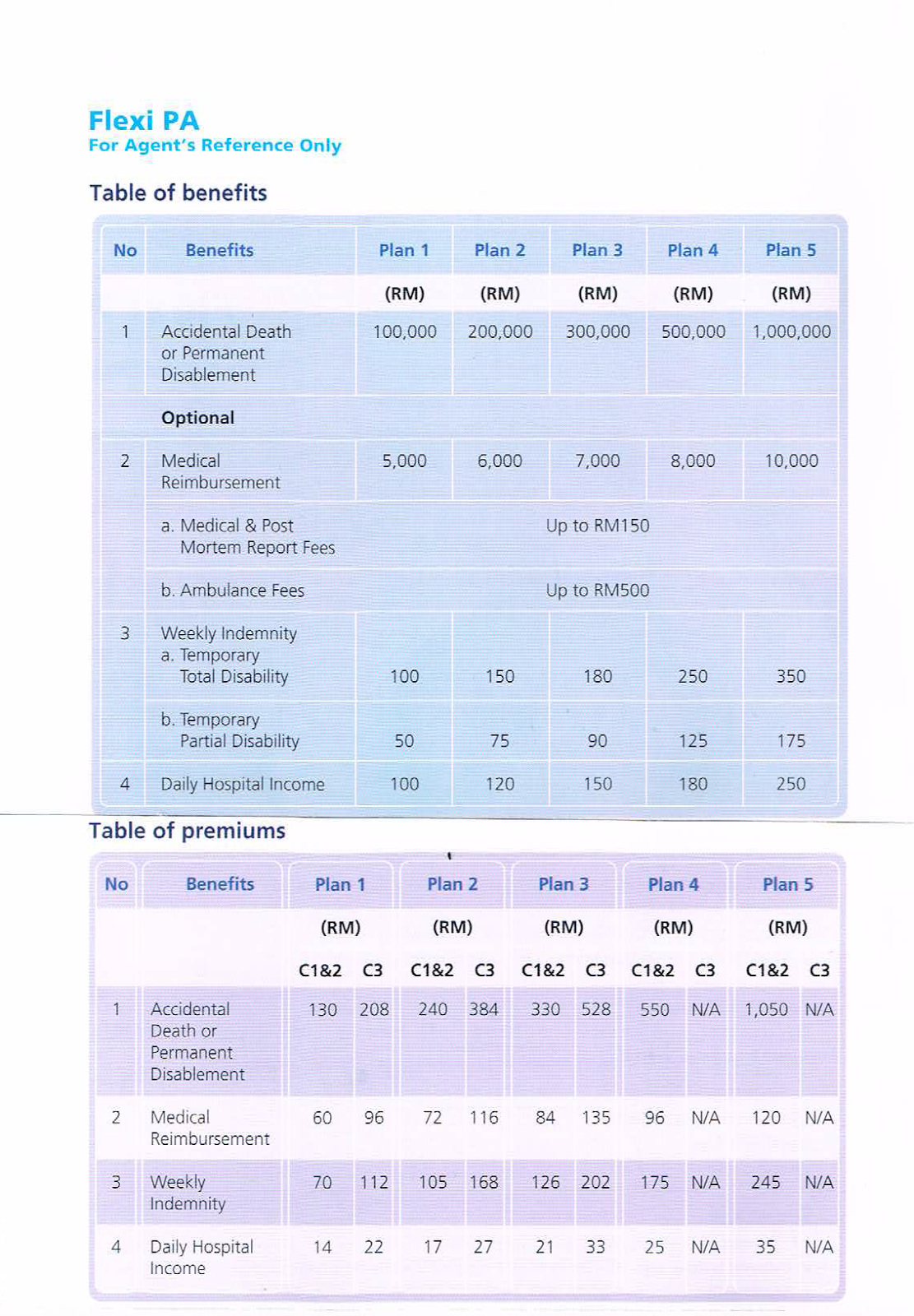

Flexi PA

1. Accidental Death

Pays the Principle Sum Insured in the event of accidental death.

2. Permanent Disablement

pays up to the Principle Sum Insured due to accident as per schedule stated in the Table of Benefits for Death and Permanent Disablement

3. Medical Reimbursement

This optional benefit will reimburse the insured as a result of an accident incurred within 52 weeks from the date of accident. This benefit will reimburse medical expense inclusive of hospital room and board, clinical, outpatient, surgical treatment due to accident and also including the following

- Medical Report/Post-mortem fee

- Ambulance fee

- Malaria, Dengue or Japanese Encephalitis

Interested contact me.

Saturday, June 24, 2017

SELAMAT HARI RAYA

May you and your family be blessed with joy and togetherness this Hari Raya.

Selamat Hari Raya, Maaf Zahir Batin.

Selamat Hari Raya, Maaf Zahir Batin.

Wednesday, May 17, 2017

Agency Meeting

Every Wednesday from 11.00 am to 12.30 pm we will have Agency Meeting cum lunch at the Cafe in the lobby of Menara Zurich Kuala Lumpur.

Asset Planner Sdn Bhd founder Encik Sarip will share very powerful and motivational speech to inspire us.

I appreciate that very much. If you think of energise your thoughts, behaviour and actions , come and join us. No obligations at all.

Asset Planner Sdn Bhd founder Encik Sarip will share very powerful and motivational speech to inspire us.

I appreciate that very much. If you think of energise your thoughts, behaviour and actions , come and join us. No obligations at all.

Tuesday, January 10, 2017

MegaMed Medical Insurance

Good News ! Finally Zurich Insurance Malaysia Berhad launched the MegaMed Medical Insurance coverage. Coverage up to Rm2.25 Million in Medical protection till age 100. The Star advertised today. This will be our current best , high coverage and comprehensive medical insurance coverage. Interested to know more please contact Tony.

Tuesday, May 31, 2016

Term Life

| ||

Zurich Term Life :

Flexible protection to safeguard those whom you cherish most.

Insurance premium is less than 3% of Sum Assured.

3 Ways to protect your hard-earned wealth.

|

Saturday, May 21, 2016

Sunday, April 24, 2016

Zurich Prowell Critical illness

Tuesday, February 23, 2016

Flex Medical

Zurich Insurance Malaysia Berhad also had this Flex Medical policy as a rider to your Investment Link Policy. Dont worry , stay protected with Flex Medical benefits. A lifetime of affordable healthcare. Attached is the details. Interested please contact me. Cheers!

Saturday, February 20, 2016

Zurich Favour8

Zurich Insurance Malaysia Berhad launch a new product . Zurich Favour8. Want to know more contact me or Zurich Sales Advisors.

Sunday, January 17, 2016

Wealth Creation

Whilst the need to accumulate savings for the future is all the more vital, Malaysians are finding it increasingly hard to fulfil their financial obligations, especially when there are retirement funds and higher education expenses to worry about . Given today's volatile economic climate , it is challenge to look for investment options that offer steady and stable return .

At Zurich Insurance , the company that I represent as Agency Manager , we take your concerns to heart when we design solutions, focusing on what matters to you. To help you acheive your financial aspirations in life, be it a comfortable retirement , quality tertiary education for your child or dream vacation , we have tailored for you Zurich Favour8.

Please contact me for more details . Terms and conditions apply .

At Zurich Insurance , the company that I represent as Agency Manager , we take your concerns to heart when we design solutions, focusing on what matters to you. To help you acheive your financial aspirations in life, be it a comfortable retirement , quality tertiary education for your child or dream vacation , we have tailored for you Zurich Favour8.

Please contact me for more details . Terms and conditions apply .

Thursday, December 24, 2015

Financial Freedom

A survey done last year by Nielsen Global Survey of Savings and Investment Strategies found that 74% of Malaysian believe that they will achieve their financial goals in future. Everyone have different financial goals such as saving for retirement , children educations, health issue, marriage, unexpected household emergencies , etc...

If you are worry and need help on your financial planning for your future goals we can help you to achieve your financial freedom.

Robert Kiyosaki best selling book , Rich Dad Poor Dad and The Cash Flow Quadrant are some methods you can apply on it.

If you are worry and need help on your financial planning for your future goals we can help you to achieve your financial freedom.

Robert Kiyosaki best selling book , Rich Dad Poor Dad and The Cash Flow Quadrant are some methods you can apply on it.

Tuesday, October 13, 2015

Zurich Omni Health

Zurich Insurance Malaysia Berhad just launch a new Medical Insurance yesterday

It is known as Zurich Omni Health. Tag line , Staying healthy has never been more rewarding.

There are a number of new features such as No Claim Bonus which gives you 10 % cash back on the premium paid.

Wellness reward Programme rewards you as you get better.Health Optimiser ofers discounts to help you stay healthy. Last but not least there is a mobile app that works like your handy personal assistant .

It is known as Zurich Omni Health. Tag line , Staying healthy has never been more rewarding.

There are a number of new features such as No Claim Bonus which gives you 10 % cash back on the premium paid.

Wellness reward Programme rewards you as you get better.Health Optimiser ofers discounts to help you stay healthy. Last but not least there is a mobile app that works like your handy personal assistant .

Monday, August 31, 2015

Retirement Disaster looms For Universal Life Policyholders

The insurance industry has a dirty little secret that threatens the retirement plans of millions of unsuspecting families.

The problem is buried in the fine print of universal life policies, widely promoted since the 1980s as a new and improved version of the old-fashioned whole life insurance product our grandparents relied on as the surest way to save for retirement.

Based on my experience as a financial advisor, most people have no idea about what they’ve already lost and will discover in time that there was no “sure” in their insurance. Instead, the insurance companies shifted their risk on to to their policyholders.

The new and improved universal whole life policies were designed to take advantage of high interest rates and growth in stock prices to reduce premiums and boost cash values—the term for the built-in savings component of a life policy.

That was the same argument the financial industry used to kill off the defined-benefit pension plans our grandparents relied on in order to sell a new generation of savers on the idea that 401-Ks had the potential for higher returns. Those higher returns might have come true had the assumptions panned out, but instead they failed in the biggest possible way.

Universal policies became attractive because they offered a higher rate of return (the dividend) on the savings component than one could get from old-fashioned whole life. The trade-off was that, unlike old-fashioned whole life, the effective premiums for the universal policy death benefit rise as the policyholder ages.

The insurance companies set a minimum premium payment based on a policyholder’s age at the time, and then used prevailing returns on stocks and bonds to argue that there would be enough profit on investments to cover both the rising premiums and the guaranteed dividend on the cash value.

In theory, the stock market would pay the added premium costs and the dividends. Millions bought universal life policies on the basis of those projections.

But most skipped the fine print, signed the papers, and squirreled them away in their safe deposit boxes where they’ve been for decades. Hidden in those policies was this potential time bomb: if the projected investment returns fail to materialize, the insurance company can make up the difference by reducing the cash value—taking money out of your cash value savings account—right down to zero, if necessary. And when that’s exhausted, they can require the policyholder to make up the difference in the death benefit premiums, or risk the policy expiring worthless.

Unlike the 1980s and 1990s when many universal policies were sold, today’s interest rates languish at historic lows. In the past 12 years the stock markets have suffered two historic collapses. For those reaching retirement age now—coupled with the housing bust and a crippled economy—this is a recipe for failure, and it’s starting to hit home.

Universal life policyholders who faithfully paid all the minimum premium payments all those years are discovering that the cash values that were to be their retirement nest eggs are nearly exhausted, and many are having to cough up huge payments just to keep the death benefit from lapsing.

For example, people who bought universal life policies when they were in their early thirties, with a $100,000 death benefit, might have faithfully paid minimum premiums of about $3,500 year in and year out thinking all was well and they were building their nest eggs. When they were younger and cheaper to insure, they were–those premiums went into the cash value buckets and earned untaxed dividends.

But as they got older, the “real” premium—the cost of insuring them—rose. A person in his or her late 50s might have a policy whose cost of insurance—the real premiums—have doubled. Five years further on, the real premium could jump to tens of thousands of dollars.

Most policyholders don’t realize they have a problem, until one day they need the cash value or discover that they will be left without even the life insurance.

How we got here is depressingly familiar in an age of financial mis-engineering. Up until the advent of universal whole life, the predominant form of life insurance for the middle class was participating—or mutual—whole life, where policyholders are treated as mutual owners of a non-public insurance company.

In such a policy, premium payments never change and accumulate like cash in a bank account earning modest dividends—guaranteed by the company—that are not taxed. Policyholders can borrow the money they paid in anytime for any purpose, no questions asked, which in turn reduces the death benefit to compensate. Policyholders can repay the loans later and the death benefits go back up again. In effect, policyholders are borrowing from and repaying themselves just as they do with any bank or investment account.

Universal life is a modern invention that takes the “sure” out of insurance by tying the benefits to the performance of stock and bond markets. In contrast, mutual whole life has ancient roots, enduring the millennia because it’s a simple and safe way to grow a nest egg while providing for one’s heirs. The practice of pooling resources this way dates as early as Roman times when people formed burial clubs to pay funeral and living expenses for member families. The earliest mutual life insurance companies in the U.S. date to the 1700s, formed by church groups to benefit their congregants in time of need.

By the mid-twentieth century, the mutual insurance industry had become the Rock of Gibraltar in the financial lives of millions of Americans. Mutual insurance companies invested their members’ premiums so conservatively that the industry survived the Great Depression intact. Those old-fashioned values have persisted and that’s why most mutual insurance companies came through the recent Great Recession with their blue-chip ratings unsullied while publicly-owned stock companies had to be bailed out to avoid bankruptcy.

I know all this because I am a reformed universal life believer. In the 1980s I became successful by helping clients replace their old reliable mutual whole life policies with the new and improved universals. By the 1990s, when some of my clients began to reach retirement age, the hidden flaws showed up when the projections fell below their targets.

I felt betrayed by the companies that had persuaded me that universal life was a better policy because stock markets historically averaged a better return. I wondered what I’d done wrong, so I went back and studied the fine print, discovering that these policies were written to shift risk from the company to the policyholder. Universal life policies allow companies to raise premiums or siphon off cash values if they can’t make enough from investments to meet their costs and still earn a profit.

That uncertainty is exactly the opposite of what whole life is supposed to accomplish—a savings nest egg that will be there no matter what happens.

Universal life policyholders who want to learn where they stand can request from their insurance companies two in-force ledger illustrations: one showing the state of the benefits at the current premium; the other showing the cost to keep a policy in force to age 100.

There are some alternatives and options for universal life policyholders, depending on how insurable they still are and other circumstances. In some cases, it’s possible to keep a policy in force at the current premium by reducing the death benefit.

For those interested in buying the right kinds of life insurance for their situations, start by determining whether a product being offered is from a mutual life insurance company that will be owned by you, or by a stockholder-owned company that is obligated above all to earn a profit for somebody else. Knowing the difference could determine the quality of your retirement.

John E. Girouard is the author of “The Ten Truths of Wealth Creation,” a registered principal of Cambridge Investment Research, and an Investment Advisor Representative of Capital Investment Advisors, in Bethesda, MD.

The problem is buried in the fine print of universal life policies, widely promoted since the 1980s as a new and improved version of the old-fashioned whole life insurance product our grandparents relied on as the surest way to save for retirement.

Based on my experience as a financial advisor, most people have no idea about what they’ve already lost and will discover in time that there was no “sure” in their insurance. Instead, the insurance companies shifted their risk on to to their policyholders.

The new and improved universal whole life policies were designed to take advantage of high interest rates and growth in stock prices to reduce premiums and boost cash values—the term for the built-in savings component of a life policy.

That was the same argument the financial industry used to kill off the defined-benefit pension plans our grandparents relied on in order to sell a new generation of savers on the idea that 401-Ks had the potential for higher returns. Those higher returns might have come true had the assumptions panned out, but instead they failed in the biggest possible way.

Universal policies became attractive because they offered a higher rate of return (the dividend) on the savings component than one could get from old-fashioned whole life. The trade-off was that, unlike old-fashioned whole life, the effective premiums for the universal policy death benefit rise as the policyholder ages.

The insurance companies set a minimum premium payment based on a policyholder’s age at the time, and then used prevailing returns on stocks and bonds to argue that there would be enough profit on investments to cover both the rising premiums and the guaranteed dividend on the cash value.

In theory, the stock market would pay the added premium costs and the dividends. Millions bought universal life policies on the basis of those projections.

But most skipped the fine print, signed the papers, and squirreled them away in their safe deposit boxes where they’ve been for decades. Hidden in those policies was this potential time bomb: if the projected investment returns fail to materialize, the insurance company can make up the difference by reducing the cash value—taking money out of your cash value savings account—right down to zero, if necessary. And when that’s exhausted, they can require the policyholder to make up the difference in the death benefit premiums, or risk the policy expiring worthless.

Unlike the 1980s and 1990s when many universal policies were sold, today’s interest rates languish at historic lows. In the past 12 years the stock markets have suffered two historic collapses. For those reaching retirement age now—coupled with the housing bust and a crippled economy—this is a recipe for failure, and it’s starting to hit home.

Universal life policyholders who faithfully paid all the minimum premium payments all those years are discovering that the cash values that were to be their retirement nest eggs are nearly exhausted, and many are having to cough up huge payments just to keep the death benefit from lapsing.

For example, people who bought universal life policies when they were in their early thirties, with a $100,000 death benefit, might have faithfully paid minimum premiums of about $3,500 year in and year out thinking all was well and they were building their nest eggs. When they were younger and cheaper to insure, they were–those premiums went into the cash value buckets and earned untaxed dividends.

But as they got older, the “real” premium—the cost of insuring them—rose. A person in his or her late 50s might have a policy whose cost of insurance—the real premiums—have doubled. Five years further on, the real premium could jump to tens of thousands of dollars.

Most policyholders don’t realize they have a problem, until one day they need the cash value or discover that they will be left without even the life insurance.

How we got here is depressingly familiar in an age of financial mis-engineering. Up until the advent of universal whole life, the predominant form of life insurance for the middle class was participating—or mutual—whole life, where policyholders are treated as mutual owners of a non-public insurance company.

In such a policy, premium payments never change and accumulate like cash in a bank account earning modest dividends—guaranteed by the company—that are not taxed. Policyholders can borrow the money they paid in anytime for any purpose, no questions asked, which in turn reduces the death benefit to compensate. Policyholders can repay the loans later and the death benefits go back up again. In effect, policyholders are borrowing from and repaying themselves just as they do with any bank or investment account.

Universal life is a modern invention that takes the “sure” out of insurance by tying the benefits to the performance of stock and bond markets. In contrast, mutual whole life has ancient roots, enduring the millennia because it’s a simple and safe way to grow a nest egg while providing for one’s heirs. The practice of pooling resources this way dates as early as Roman times when people formed burial clubs to pay funeral and living expenses for member families. The earliest mutual life insurance companies in the U.S. date to the 1700s, formed by church groups to benefit their congregants in time of need.

By the mid-twentieth century, the mutual insurance industry had become the Rock of Gibraltar in the financial lives of millions of Americans. Mutual insurance companies invested their members’ premiums so conservatively that the industry survived the Great Depression intact. Those old-fashioned values have persisted and that’s why most mutual insurance companies came through the recent Great Recession with their blue-chip ratings unsullied while publicly-owned stock companies had to be bailed out to avoid bankruptcy.

I know all this because I am a reformed universal life believer. In the 1980s I became successful by helping clients replace their old reliable mutual whole life policies with the new and improved universals. By the 1990s, when some of my clients began to reach retirement age, the hidden flaws showed up when the projections fell below their targets.

I felt betrayed by the companies that had persuaded me that universal life was a better policy because stock markets historically averaged a better return. I wondered what I’d done wrong, so I went back and studied the fine print, discovering that these policies were written to shift risk from the company to the policyholder. Universal life policies allow companies to raise premiums or siphon off cash values if they can’t make enough from investments to meet their costs and still earn a profit.

That uncertainty is exactly the opposite of what whole life is supposed to accomplish—a savings nest egg that will be there no matter what happens.

Universal life policyholders who want to learn where they stand can request from their insurance companies two in-force ledger illustrations: one showing the state of the benefits at the current premium; the other showing the cost to keep a policy in force to age 100.

There are some alternatives and options for universal life policyholders, depending on how insurable they still are and other circumstances. In some cases, it’s possible to keep a policy in force at the current premium by reducing the death benefit.

For those interested in buying the right kinds of life insurance for their situations, start by determining whether a product being offered is from a mutual life insurance company that will be owned by you, or by a stockholder-owned company that is obligated above all to earn a profit for somebody else. Knowing the difference could determine the quality of your retirement.

John E. Girouard is the author of “The Ten Truths of Wealth Creation,” a registered principal of Cambridge Investment Research, and an Investment Advisor Representative of Capital Investment Advisors, in Bethesda, MD.

Thursday, July 9, 2015

Umbrella for protection

Sunday, May 17, 2015

D.I.Y. Insurance

If you think of buying insurance , what will you do ?

Search the Internet / Google insurance to find out more information's ?

Or call your current Insurance Advisor and if no Insurance Advisor / Agents will you ask

for some referrals ?

I came across this D.I.Y insurance advertisement in the newspaper recently , will you do it yourself ?

I believe insurance must be sold . That's mean you need to facts find like what

is the current needs and amount of insurance need and what are the risks that

the person is looking for ? Example , medical insurance , living assurance such as

dread diseases , long term care , total permanent or premature death benefits ?

Please give us your feedback . Thank You.

Search the Internet / Google insurance to find out more information's ?

Or call your current Insurance Advisor and if no Insurance Advisor / Agents will you ask

for some referrals ?

I came across this D.I.Y insurance advertisement in the newspaper recently , will you do it yourself ?

I believe insurance must be sold . That's mean you need to facts find like what

is the current needs and amount of insurance need and what are the risks that

the person is looking for ? Example , medical insurance , living assurance such as

dread diseases , long term care , total permanent or premature death benefits ?

Please give us your feedback . Thank You.

Tuesday, November 4, 2014

Medical Insurance for MM2H

MALAYSIA MY SECOND HOME (MM2H) PROGRAM - 10 YEARS MALAYSIA VISA RENEWAL FOR A LIFETIME !

MALAYSIA MY SECOND HOME (MM2H) PROGRAM - 10 YEARS MALAYSIA VISA RENEWAL FOR A LIFETIME ! WHY MALAYSIA ? Government Support / Rule of Law / High Standard Living / Low Cost Living / Pleasant Weather / Affordable Quality Home

WHY MALAYSIA ? Government Support / Rule of Law / High Standard Living / Low Cost Living / Pleasant Weather / Affordable Quality Home

No Natural Calamities / Good Infrastructure / Political Stability / Quality Education & Medical Facilities / Recreation & Entertainment / Rich Culture

Multi Racial Friendly English Speaking People / Variety Food & Fruits / High Class Shopping / Window to Asia

MAIN BENEFITS OF MM2H PROGRAM � Conditional Approval in 6 Weeks+ & 6 Months To Endorse MM2H Visa to your Passport !

Malaysia requires foreigners who are applying for the Malaysia My 2nd Home (MM2H) Programme to have medical insurance taken in Malaysia.

Zurich Insurance Malaysia Berhad would like to propose an attractive plan called Zurich ML210 for foreigners planning to take MM2H or to those who are simply seeking medical coverage here in Malaysia.

Please contact Tony at +603-21469226 or email:ttong3@gmail.com

Subscribe to:

Posts (Atom)